One Trillion Dollars

Q1 2023 Monetary Stimulus One for the Books

Financial markets are off to a hot start in 2023:

BTC: +70%

NDX: +21%

XAU: +8%

TLT: +7%

SPX: +7%

But isn’t inflation at decades-highs? Isn’t the Fed raising rates? Isn’t the housing market in the shitter? Why the heck are financial markets pumping?

Simple: The US government is pumping our bags.

Don’t get too complacent though… this won’t last forever. Read on for why.

Why Markets Are Pumping

Firstly and most simply, the economy continues to do quite well.

Despite endless hand-wringing from market commentators and cautious outlooks from US corporates, Q1’23 real GDP is on track for positive 2.5% growth according to the Atlanta Fed, far from recessionary. Markets were conservatively positioned entering the year and failure of fundamental data to roll over has led market participants to re-enter risky assets.

Secondly and less appreciated, global financial markets have benefitted from immense monetary stimulus from the US Federal Government to start the year.

Two unexpected developments have led the Fed to unintentionally “pump” markets year-to-date: (1) The Bank Crisis and (2) The Debt Ceiling.

(1) The Bank Crisis: The Silicon Valley Bank bank run that began on March 9th kicked off a crisis of confidence in the global banking system. Over the past few weeks we’ve seen the #2 and #3 largest bank failures in history - Silicon Valley Bank and Signature Bank - and the emergency marriage of two of Europe’s largest banks - Credit Suisse and UBS.

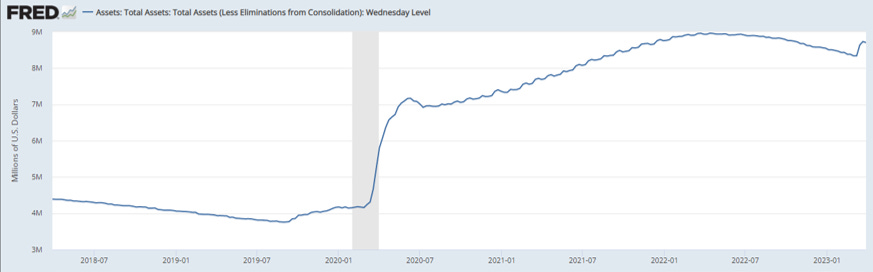

In response to the banking crisis, the Fed created the Bank Term Funding Program (BTFP), whereby banks could pledge their securities to the Fed in exchange for credit to plug the hole left by fleeing depositors. BTFP plus other programs caused the Fed’s balance sheet to grow by roughly $400 billion in a couple of weeks, the largest monthly increase since March 2020 during the COVID stimulus blowout.

The Bank Crisis Nearly Reversed All of the Fed’s Quantitative Tightening

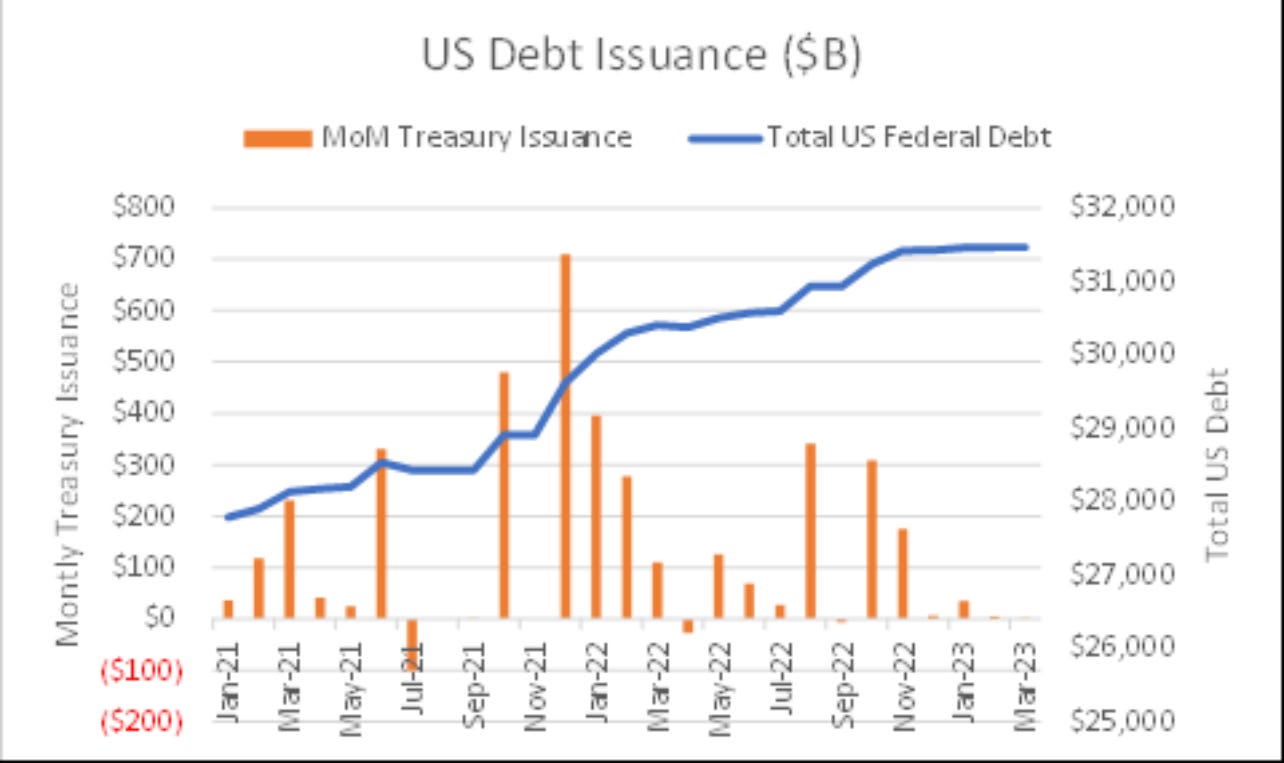

(2) The Debt Ceiling: Beginning in December, the US Government ran into its arbitrary ~$31.4 trillion cap on Federal government debt. Since then, the US Treasury has ceased issuing treasuries. To cover the US government’s deficit while US Congress haggles over raising the debt ceiling, the US Treasury has been draining the Treasury General Account (TGA), the US government’s operating account. The TGA has dropped by $276 billion over the past few months and currently sits at $184 billion. New Capital Management estimates that extraordinary measures by the US Treasury could provide up to $950 billion in available funds to meet government obligations through the summer.

Draining the TGA in lieu of issuing US Treasuries has a stimulative effect on financial markets. That’s $1 trillion coming out of the Treasury’s coffers *instead* of financial markets. Said another way, given the Treasury is unlikely to be issuing treasuries through the first half of 2023, up to $1 trillion of capital that would otherwise be buying primary treasury issuance is now freed up to buy other financial assets, such as treasuries on secondary markets, tech stocks, and even crypto.

US Debt Issuance is Temporarily at $0 Until the US Resolves its Debt Ceiling

Where We Go from Here

Between the increase in the Fed’s balance sheet and draining the TGA, monetary assets have received >$500 billion of stimulus YTD and likely well over a trillion dollars on an annualized basis. Big.

For the next few months, the market backdrop is probably more mixed but leans favorable. The Fed’s balance sheet has resumed declining as the banking crisis cools and Quantitative Tightening (QT) resumes. However to the extent the Treasury continues to tap the TGA, lack of treasury issuance will be a tailwind for financial markets.

However, beginning in the summer things start to look shakier.

Once the debt ceiling is resolved the Fed will re-enter the market with treasury issuance. The US Congressional Budget Office (CBO) projects the US budget deficit will be around $1.4 trillion in 2023, grow to $1.6 trillion in 2024, and continue growing thereafter. That’s a lot of paper that the market has to absorb. This will likely put upward pressure on rates and pose a headwind to financial assets.

As I wrote in my first long-form Substack “Why the 1% Don’t Get It,” I believe the end-game is yield curve control and significant dollar debasement. Until then financial markets are likely to remain turbulent.

Further compounding the risks facing the market, excess consumer savings created during COVID are likely drained around the middle of this year. For a sober assessment of the headwinds facing the markets in 2023, highly recommend this tweet from market expert KKGB Kitty:

It’s Not All Doom and Gloom

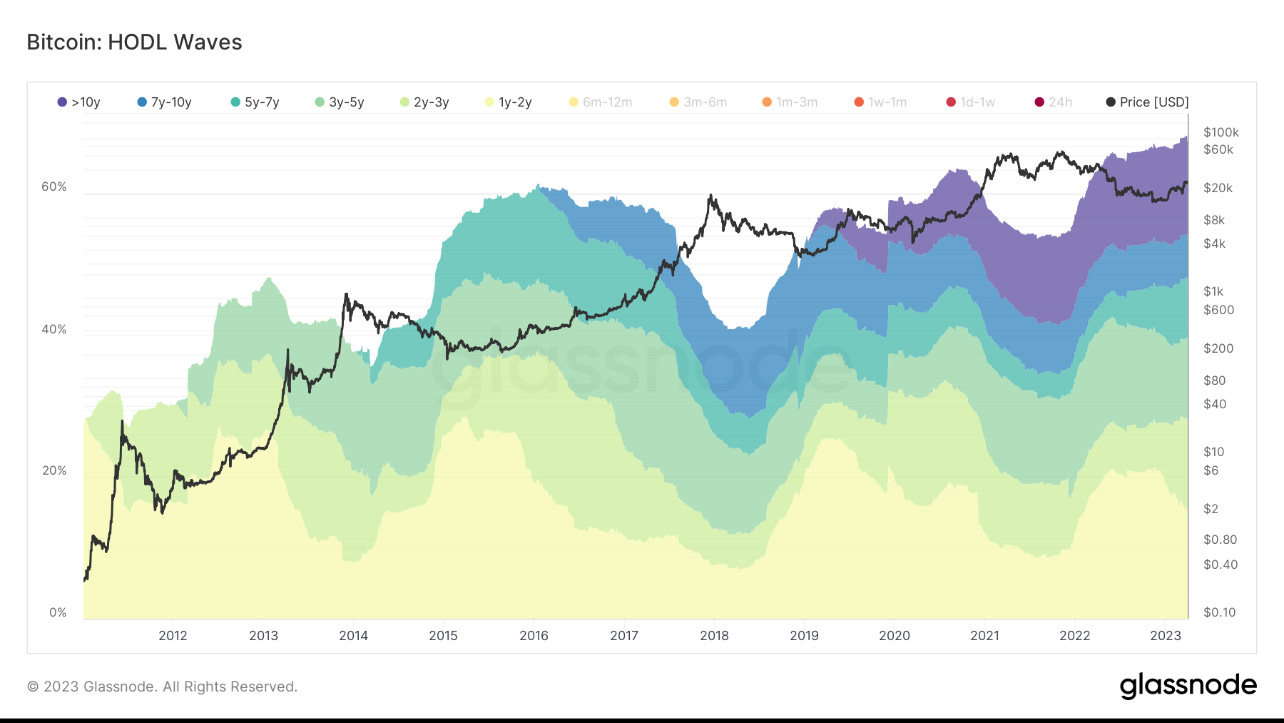

Offsetting the headwinds facing the market around the middle of the year, bitcoin HODLer data looks CRAZY BULLISH. This and continued tailwinds from the debt ceiling deadlock is keeping me from being overly bearish on crypto in the near-term. However, if we do finally begin rolling into a recession later this year I suspect risk assets will struggle.

Bitcoin Long-term Holders Keep Making New All-time Highs

Whatever happens over the coming months, it will no doubt be interesting.

If you’re in the market for a sick hat and love spreading aloha, check out Aloha Lidz.

Writing takes an immense amount of time and effort. You can further support my work by:

(For traders) Using my ref link for 10% off trades on GMX, crypto’s #1 trading platform: http://app.gmx.io/?ref=808trades

(For everyone else): Making a smol donation via my ETH wallet: 0x8Ab68C848749956e9F26d8a76C1FCB60817366c1